News & Resources

COVID-19 Business Planning

November 23, 2020 update:

October 19, 2020 update:

September 3, 2020 update:

August 31, 2020 update:

August 7, 2020 update:

July 7, 2020 update:

June 10, 2020 update:

June 5, 2020 update:

May 13, 2020 update:

May 7, 2020 update:

May 4, 2020 update:

April 30, 2020 update:

April 22, 2020 update:

April 15, 2020 update:

April 13, 2020 update:

April 11, 2020 update:

-

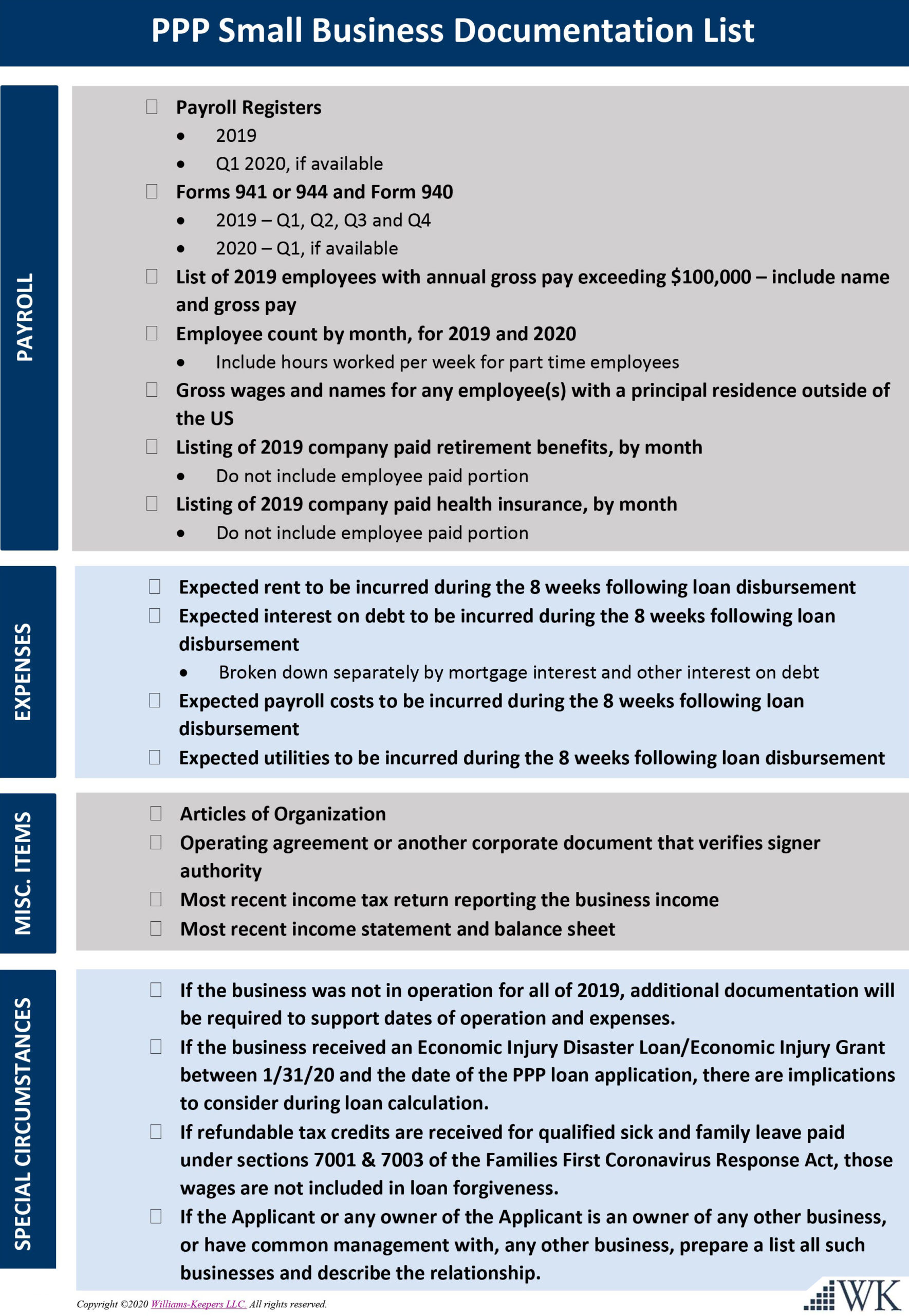

Applying for the PPP? Here’s what you need

-

How to Claim NOL Carrybacks and Enhanced Carryforwards

-

IRS extends Q2 estimated payment due date, more tax deadlines for estates, trusts, other entities

-

Details Lacking as PPP Expands to Include Self-Employed Taxpayers, Independent Contractors

-

New lending programs available for larger businesses, local governments

April 3, 2020:

NOVEMBER 23, 2020 UPDATE:

IRS Releases Additional Guidance on Deductibility of PPP Loan Expenses

The United States Treasury provided highly anticipated Paycheck Protection Program (PPP) loan forgiveness guidelines last week (the press release is available here). According to the Internal Revenue Services(IRS), Congress failed in its effort to make PPP funds truly tax free by requiring borrowers benefitting from loan forgiveness to treat PPP-funded costs as non-deductible. The new guidance states the tax impact of the non-deductible costs will be recognized in the year the costs are paid and incurred, not the year forgiveness is requested.

As a result, many borrowers who were waiting to submit forgiveness applications until 2021 can move forward with applications in 2020 without affecting the timing of the non-deductibility. Also, most sole proprietor and partnership borrowers will want to claim the maximum amount of owner self-employment income replacement on forgiveness applications, as PPP expenditures for these items should not be subject to the same taxation problem.

We still hold some hope Congress will act to restore its original intent: that PPP funds are truly non-taxable. As we have done since early this year, we will continue to monitor legislation and regulatory guidance on this issue.

Also, for borrowers who received PPP loans in excess of $2 million we continue to monitor changes to a new questionnaire the SBA intends to use to make hindsight determinations regarding whether the loan was “necessary.”

In the meantime, do not hesitate to reach out to your WK advisor to discuss how WK can help your business navigate the PPP forgiveness process.

OCTOBER 19, 2020 UPDATE:

SBA Releases simplified PPP forgiveness application for borrowers of $50,000 or less

On October 8 the Small Business Administration (SBA) released a new Paycheck Protection Program (PPP) loan forgiveness application, Form 3508S (available on the IRS website here). This form, directed at borrowers who received loans of $50,000 or less, is intended to be a further simplified application that requires fewer calculations and documentation to receive loan forgiveness.

One of the biggest advantages to using Form 3508S is that eligible borrowers are exempt from any reduction in loan forgiveness based on reductions in full-time-equivalent (FTE) employees or reductions in employee wages. Eligible borrowers are also not required to report any employee information on the application or to show the calculations used to determine their loan forgiveness amount. However, they do still need to provide their lender with payroll information and other supporting documentation necessary to substantiate the costs claimed for forgiveness. Eligible borrowers should also be prepared for any additional requests for information from the IRS as part of their review process.

A fourth phase of COVID relief, which will likely contain provisions that impact the PPP forgiveness process, is being debated in Congress. Although negotiations appear to be at a standstill, various proposals have provided for “automatic” forgiveness for borrowers who received loans of $150,000 or less. Borrowers whose loans total less than $50,000 and wish to get off the PPP rollercoaster may consider completing this new Form 3508S application, despite the possibility that an automatic forgiveness threshold could be reached by proposed legislation.

Many lenders are not yet accepting or processing forgiveness applications and borrowers have up to 10 months after the end of their covered period before any payments are due, so a wait-and-see approach over the coming weeks or months might be the best choice for businesses with $50,000 or less in PPP loans. If your business received a PPP loan between $50,000 and $150,000 it would make sense – barring an extenuating circumstance such an impending sale of the business – to wait to apply for forgiveness as the loan might eventually be subject to automatic forgiveness.

Additionally, although the forgiven loan is not taxable income to the borrower, any expenses funded with forgiven PPP proceeds are non-deductible under present law. Members of Congress have expressed a desire to pass legislation to make the expenses deductible, and that issue will likely also be addressed in the next round of COVID-relief legislation. Until this issue is “fixed” by legislation, many businesses owners might wish to delay forgiveness until 2021 in case the Treasury releases favorable rules that might allow these disallowed deductions to be taken into consideration in the year of forgiveness (2021) instead of the year the funds were expended (2020).

SEPTEMBER 3, 2020 UPDATE:

Payroll Tax Deferral Update

Having received some questions about the update provided by WK on Monday, August 31, we would like to provide clarification about recently released IRS guidance on the payroll tax deferral created by the August 8, 2020 executive order from President Donald Trump.

Among many unanswered questions in the IRS guidance, the one thing that is clear is that the burden of risk is on the employer to pay back any employee social security taxes deferred between September 1, 2020 and December 31, 2020, and that repayment is to take place during first four months of 2021. According to the notice, the business “may make arrangements to otherwise collect the total Applicable Taxes from the employee,” but no further guidance is given about how that would work.

Although there is little in the way of definitive guidance provided, it appears that the deferral is not mandatory, and the business, not the employee, has the ultimate say in whether to participate.

Most businesses will be hesitant to participate and make the deferral because these taxes are not currently scheduled to be forgiven, and Congress has not expressed an intention to provide forgiveness. Additionally, questions surrounding the mechanism for repayment, particularly in situations where employees leave prior to the repayment period, will give businesses further reason to not participate at this time.

The risk of not participating is that these taxes are eventually forgiven and forgiveness is missed on taxes paid from September 1 until date forgiveness is announced. Given the uncertainty surrounding forgiveness, however, it appears reasonable for businesses to wait to opt into the program until forgiveness is guaranteed.

WK will continue to provide additional guidance as more information is released. If you have any questions regarding your specific situation in the meantime, please contact your WK advisor.

AUGUST 31, 2020 UPDATE:

Questions remain for executive order’s new payroll withholding guidelines

An executive order (linked) issued by President Donald Trump on August 8, 2020 allows employers to defer withholding, deposit, and payment of the employee portion of social security taxes (6.2 percent) on wages paid between September 1, 2020 and December 31, 2020. The executive order was aimed at providing relief as a result of the COVID-19 pandemic, but it also creates several important questions about its potential impact on employers.

In accordance with the order, employee wages are only eligible for the deferral if they are less than $4,000 per bi-weekly pay period, or the equivalent threshold amount with respect to other pay periods (the equivalent of $104,000 annually) and if employers opt into the deferral. Please note the deferral is just that, a delay in timing of the payment until the beginning of 2021, not forgiveness of the tax due.

The Department of the Treasury and Internal Revenue Service issued guidance on August 28, 2020 to help address questions related to the deferral, but many details have not been clarified. Specifically, questions remain related to employer risk if employees leave without repayment, whether the tax deferral ultimately be forgiven and the application of penalties related to filing.

The American Institute of Certified Public Accountants (AICPA) has issued a directive for clarification to the Department of the Treasury. However, because Congress is currently in recess until September 8, answers are not expected until after that time.

What should employers do while waiting for answers? The most conservative approach is to allow employees to opt into the program, deferring social security taxes if eligible employees opt in. However, there are valid concerns with regard to implementation, risk associated with employer tax penalties and repayment by employees that will lead many employers to choose not to implement the deferral. In this time of uncertainty related to the issue, the burden of risk is placed on the employer should they choose to proceed at this time.

WK will continue to provide additional guidance as more information is released. If you have any questions regarding your specific situation in the meantime, please contact your WK advisor.

AUGUST 7, 2020 UPDATE:

Is your COVID-19-related assistance subject to an audit?

Certain COVID-19-related assistance programs could be subject to an audit under the Office of Management and Budget’s (OMB) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (the Uniform Guidance (UG)). Regardless of whether an organization is a for- or not-for-profit entity, this could trigger its first audit.

The UG applies to the following COVID-19-related assistance programs.

- CFDA #16.034 – Justice Coronavirus Emergency Supplemental Funding Program

- CFDA #21.019 – Treasury Coronavirus Relief Fund

- CFDA #32.006 – Federal Communications Commission COVID-19 Telehealth Program

- CFDA #59.008 – Small Business Administration (SBA) Disaster Assistance Loans (Economic Injury Disaster Loans)

- CFDA #84.184C – Education CARES Act Project SERV

- CFDA #84.425 – Education Stabilization Fund

- CFDA #93.461 – Health and Human Services (HHS) Uninsured COVID Testing and Treatment

- CFDA #93.498 – HHS Provider Relief Fund

- CFDA #93.527 – HHS Grants for New and Expanded Services Under the Health Center Program

- CFDA #93.665 – HHS Emergency Grants to Address Mental and Substance Use Disorders During COVID-19

- CFDA #93.697 – HHS Rural Health Clinic Testing

For-profit entities expending $750,000 or more of these funds during its fiscal year will be subject to an audit under the UG, either 1) a financial-related audit of a particular award or multiple programs in accordance with Government Auditing Standards or 2) a full Single Audit.

Not-for-profit entities expending $750,000 or more of these funds during its fiscal year will be subject to a full Single Audit under the UG.

Single Audits are performed in accordance with Government Auditing Standards, which require more testing and reporting than a normal audit. Single Audits are required to be submitted to the Federal Audit Clearinghouse within nine months after the entity’s fiscal yearend (or within 30 days of the audit report date, whichever comes first).

The UG does not apply to the following COVID-19-related assistance programs.

- CFDA #10.130 – Agriculture Coronavirus Food Assistance Program

- CFDA #21.018 – Treasury Coronavirus Relief: Pandemic Relief for Aviation Workers

- CFDA #59.072 – SBA Economic Injury Disaster Loan Emergency Advance

- CFDA #59.073 – SBA Paycheck Protection Program

- CFDA #59.074 – Office of Entrepreneurial Development Resource Partners Training Portal

Expenditures of these funds should not be included in the entity’s calculation of the $750,000 threshold trigging an audit.

WK can help you determine whether your COVID-19-related assistance could be subject to an audit. Please contact your WK advisor to learn more about how we can help you ensure compliance with these new requirements.

JULY 7, 2020 UPDATE

Paycheck Protection Program Loan Application Deadline Extended

President Trump signs extension of time for Paycheck Protection Program loan applications

On Saturday, July 4, President Trump signed into law an extension of time for eligible businesses to apply for Paycheck Protection Program (PPP) loans. The bill passed both the Senate and the House via unanimous consent votes earlier that week.

For any business that assumed they were not eligible or otherwise declined to pursue a PPP loan, the deadline to apply has been extended from June 30, 2020 to August 8, 2020.

SBA and Treasury release detail on PPP loans and borrowers

On Monday, July 6, the Small Business Administration (SBA) and the Department of Treasury (Treasury) released loan data on the 4.9 million PPP loans that have been made to date. The loan-level data in the release includes business names, addresses, NAICS codes, zip codes, business type, demographic data, non-profit information, name of lender, jobs supported, and loan amount ranges as follows:

- $150,000-350,000

- $350,000-1 million

- $1-2 million

- $2-5 million

- $5-10 million

For all loans below $150,000, SBA is releasing all of the above information except for business names and addresses. You can see the release from SBA and Treasury here.

JUUNE 10, 2020 UPDATE:

U.S. Treasury and U.S. Small Business Administration Release Joint Statement on the Paycheck Protection Program Flexibility Act and Provide Guidance on the 60% Payroll Rule

On Monday, June 8, Treasury Secretary Steven Mnuchin and Small Business Administration (SBA) Administrator Jovita Carranza issued a joint statement on the enactment of the Paycheck Protection Program Flexibility Act (Flexibility Act). As noted in our June 5 update, the Flexibility Act made changes to the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), including an extension of time from eight weeks to 24 weeks to spend Paycheck Protection Program (PPP) loan proceeds on what we have termed “good costs.”

In addition, the Flexibility Act changed the requirement created by Treasury and the SBA that 75 percent of a business’ requested loan forgiveness must be supported by payroll costs, thus limiting the amount of non-payroll good costs that a business could count toward forgiveness. The Flexibility Act liberalized the rule by reducing the percentage from 75 percent to 60 percent. However, the way the Flexibility Act was drafted appeared to create a “cliff” where one previously did not exist. Specifically, the 75 percent rule only served to limit the amount of non-payroll costs eligible for forgiveness. The new 60 percent rule appeared to preclude a business from receiving any forgiveness if it did not expend at least 60 percent of its PPP loan proceeds on payroll costs.

The joint Treasury/SBA statement clarifies that the 60 percent rule will not be interpreted as a “cliff.” Instead, the mechanics of the new 60 percent rule will mirror those applicable to the old 75 percent rule, and partial forgiveness will be available for those businesses that do not meet the 60 percent rule.

As noted in our June 5 update, other unanswered questions remain. In the joint statement, SBA and Treasury state they will “promptly issue rules and guidance, a modified borrower application form, and a modified loan forgiveness application implementing these legislative amendments to the PPP.” WK will continue to monitor the release of additional guidance and will provide updates as necessary.

WK plans to provide a video update to the May 27 PPP webinar to discuss the changes in the Flexibility Act and related guidance. In the meantime, do not hesitate to reach out to your WK advisor to discuss how WK can help your business navigate the PPP forgiveness process.

JUNE 5, 2020 UPDATE:

Congress Changes Rules for PPP Loans to Increase Flexibility, But Leaves Many Unanswered Questions

President Donald Trump signed into law today the Paycheck Protection Program Flexibility Act (the Flexibility Act), which modified key provisions in March’s Coronavirus Aid, Relief, and Economic Security Act (CARES Act). The new legislation’s primary changes impact loan forgiveness under the Paycheck Protection Program (PPP).

Businesses now have 24 weeks to spend PPP loan proceeds on what we have termed “good costs.” However, businesses may elect to retain the eight-week period provided in the original program, and should do so if their loan qualifies for full forgiveness to guard against wage or employee reductions that could occur after the eight-week period has expired but before the 24-week period expires. The 24-week period would be cut short if the 24-week period would extend beyond December 31, 2020, which should not be an issue for businesses that have already received PPP funding. The December 31, 2020 date will be relevant for any business that receives its first PPP funds in July or later.

To qualify for full forgiveness, businesses generally must maintain full-time equivalent employee (FTE) counts and refrain from certain reductions in pay rates for employees. For businesses making use of the 24-week period, they generally must also maintain baseline FTE counts and pay rates for the full 24-week period. The Flexibility Act leaves unchanged the computation for baseline FTE counts and baseline pay rates.

If a business fails to maintain its baseline FTE counts or baseline pay rates, it still has an opportunity to qualify for maximum forgiveness by restoring FTE counts or pay rates before the specified measurement date. The measurement date for all businesses to test whether they have restored their FTE count or pay rates for certain employees has been moved from June 30, 2020 to December 31, 2020. The Flexibility Act also provides additional statutory relief to the extent FTE reductions resulted from either of two situations:

- the business tried to rehire those employed on February 15, 2020 but could not and was unable to hire “similarly qualified” employees on or before December 31, 2020; or

- the business can document an inability to return to its February 15, 2020 level of business activity due to compliance with HHS, CDC, or OSHA requirements or guidance related to the maintenance of any worker or customer safety requirement related to COVID (e.g., standards for sanitation or for social distancing).

The Flexibility Act addresses the 75 percent requirement the United States Treasury (Treasury) and the Small Business Administration (SBA) previously created, under which at least 75 percent of a business’ requested loan forgiveness must be supported by payroll costs, thereby restricting the extent to which non-payroll costs (i.e., mortgage interest, rent, utilities) could be used to support a forgiveness application. That rule was not contained in the CARES Act but was provided by Treasury and SBA to help to allocate scarce PPP resources.

The Flexibility Act adds a statutory requirement that both liberalizes and tightens the rule. The Flexibility Act liberalizes the threshold by reducing it from 75 percent to 60 percent; however, it seems to create a “cliff” through which a business must spend 60 percent or more of the funds it received for payroll costs to receive any loan forgiveness. Senator Marco Rubio (R-FL) has commented on his discomfort with the apparent cliff effect and has invited SBA guidance to soften it.

Most businesses have a better chance of achieving full loan forgiveness as a result of the Flexibility Act, but not all will. For new loans, the Flexibility Act has lengthened the minimum maturity from two years to five years, but this change does not apply to existing PPP loans, though refinancing the two-year loans may be possible. The Flexibility Act generally defers principal, interest, or fees collected on PPP loans until the amount of forgiveness is determined and paid by the federal government to the lender. The Flexibility Act also addresses what happens if a borrower does not timely file for forgiveness. A filing will be timely if it occurs within 10 months following the expiration of the 24-week period (or, for loans made in July or later, December 31, 2020).

Finally, the CARES Act included an incentive to allow certain businesses to defer paying the employer’s share of 2020 social security taxes, with half due at the end of 2021 and the other half due at the end of 2022. However, the deferral was truncated upon PPP loan forgiveness. The Flexibility Act now allows businesses receiving PPP loan forgiveness to qualify for this deferral.

When assessing the impact of the Flexibility Act and how it applies to them, business owners should consider these action items.

- Continue to measure “good costs” and FTEs during the eight-week period beginning the date the first PPP loan was funded. If you spend 100 percent of the proceeds on good costs, spend at least 60 percent on payroll, had no reduction in FTEs and did not reduce pay for your employees, then you can and should file for forgiveness later this summer based on existing PPP guidance.

- If full forgiveness is not likely based on the eight-week period, then businesses should expand cost measurement and tracking of FTEs to the 24-week period and to evaluate whether FTE counts or pay rates can be restored by December 31, 2020 and whether the aforementioned new statutory relief provisions might apply to excuse any FTE shortfall.

- Businesses whose loans were capped by their banks based on expected eight-week “good costs” should discuss with their banks a possible application for additional PPP funds.

- Defer payment of payroll taxes.

As might be expected, late rule changes raise new questions that will need to be considered. For example, we do not know:

- when the forms will be available to request PPP loan forgiveness, and whether those electing the eight-week period will be allowed to apply earlier than those using the new default 24-week period;

- whether the favorable guidance on accrued but unpaid costs devised for the eight-week period will be applied to the 24-week period;

- whether guidance allowing 8/52nds of certain costs to be counted will be frozen at 8/52nds or expanded to 24/52nds; and

- whether Treasury will soften the “cliff” effect if a business spends more than 40 percent on non-payroll good costs (i.e., mortgage interest, rent, and utilities).

Williams-Keepers LLC has a team of experienced advisors evaluating how the legislation affects the firm’s clients and the business decisions they face.

MAY 13, 2020 UPDATE:

SBA offers critical PPP guidance on borrower certifications

- [C]urrent economic uncertainty makes this loan request necessary to support the ongoing operations of the Applicant.

Our May 4 post identified the confusion created whether businesses that had theoretical access to other capital sources must exhaust those sources before qualifying for Paycheck Protection Program (PPP) loans. Today the SBA today released the following clarifications, all of which relieve stress created by prior guidance.

- Safe harbor for small loans. For loans less than $2 million (aggregated to include loans to all affiliated companies), the SBA has created a safe harbor through which these businesses are deemed to have met the “necessary” requirement automatically. We recommend clients retain documentation supporting the necessity of the loans, but additional efforts to document economic risks faced are unlikely to be needed.

- Guidance for large loans. Although no safe harbor exists for loans $2 million or greater, businesses should document the reasons the loan was necessary. Under the new guidance, if the SBA later disagrees with a business’ determination the loan was necessary, then the business can avoid feared civil or criminal exposure by promptly repaying the loan at that time. This guidance alleviates much of the stress felt by some recipients of larger PPP loans whether to repay the loans before tomorrow’s May 14, 2020 deadline.

The May 14, 2020 repayment deadline is still relevant if a business received a PPP loan greater than $2 million and it does not believe it can demonstrate that loan was necessary. Businesses who repay the funds before May 14 may qualify for the employee retention 50 percent income tax credit for wages paid to employees. The Coronavirus Aid, Relief, and Economic Security (CARES) Act authorized both the employee retention credit and PPP loans, but required businesses to choose between the two. As a result, only businesses with larger loans and significant doubts whether they qualify, or businesses now concerned about reputational impacts of PPP loans will need to consider repaying their PPP loans on May 14.

Please contact your WK advisor for additional information about how the new guidance might affect your specific situation.

MAY 7, 2020 UPDATE:

IRS publishes procedure to return stimulus payments paid in error to deceased taxpayers

The United States Congress provided for $1,200 payments to most citizens in the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) to help households navigate the COVID-19 pandemic. In an attempt to distribute the funds quickly, payments were sent to individuals who did not qualify, including deceased taxpayers, leaving families of the recently deceased unsure what they need to do with the proceeds. Some of these payments were made electronically, further complicating this question.

On May 6, the Internal Revenue Service (IRS) published its protocol for returning funds received in error.

If the payment was a paper check:

- write “Void” in the endorsement section on the back of the check;

- mail the voided Treasury check immediately to the appropriate IRS location published here: https://www.irs.gov/coronavirus/economic-impact-payment-information-center#eligibility (Q&A #41);

- do not staple, bend or paper clip the check; and

- include a note stating the reason for returning the check.

If the payment was a paper check and you have cashed it, or if the payment was a direct deposit:

- submit a personal check, money order, etc., immediately to the appropriate IRS location published here: https://www.irs.gov/coronavirus/economic-impact-payment-information-center#eligibility (Q&A #41);

- write on the check/money order made payable to “U.S. Treasury” and write 2020EIP, and the taxpayer identification number (social security number, or individual taxpayer identification number) of the recipient of the check; and

- include a brief explanation of the reason for returning the EIP.

For Missouri-resident decedents, returned stimulus checks can be mailed to the IRS using the following address.

Kansas City Refund Inquiry Unit

333 W Pershing Rd

Mail Stop 6800, N-2

Kansas City, MO 64108

For living taxpayers, the determination of eligibility is generally based on gross income in 2018 or 2019, depending on whether the 2019 return has been filed, or in 2020. The income thresholds, or adjusted gross income(AGI), for payment follow.

- Single or Married filing separately: $75,000 full benefit, fully phased out at $99,000

- Head of Household: $112,500 full benefit, fully phased out at $136,500

- Married filing jointly: $150,000 full benefit, fully phased out at $198,000

Because some could qualify in only one of these periods and because Congress did not include a mechanism to claw back funds based on income increases in 2019, some taxpayers have intentionally delayed filing their 2019 returns to ensure the United States Treasury uses 2018 income figures. For those who will qualify for a larger benefit based on 2020 income than on 2018 or 2019 income, they will receive the larger 2020 benefit but will need to wait until next spring to receive the funds.

MAY 4, 2020 UPDATE:

SBA Updates Q&A to Address Paycheck Protection Program Eligibility

The Paycheck Protection Program (PPP), one of the major COVID-relief measures for businesses included in the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), has provided more than $500 billion in forgivable loans since its rollout on April 3, 2020. The program, however, has been plagued by confusion about the mechanics of how the loan forgiveness will work, as well as disagreements on whether the funds are getting to those who need them the most.

This discussion has recently turned to the qualifications for receipt of a PPP loan and, specifically, the certifications necessary to obtain a loan. This confusion is a product, at least in part, of the rapid implementation of the program, as well as the evolving economic and political environment.

At the outset, all small businesses were encouraged to participate in the program. United States Treasury Secretary Steven Mnuchin, on Fox News Sunday on March 29 (the Sunday before the PPP rollout) reiterated this position: “I encourage all small businesses to take out these loans because if you hire back your workers for eight weeks, you’ll have a forgivable loan and the government will pay for that.”

Consistent with a “big tent” approach, the definition of a “small business” for purposes of the PPP was expanded to be more inclusive than the standard definition under the Small Business Administration (SBA). In addition to the normal qualifications, the definition was expanded to include businesses with 500 or fewer employees, and in the case of hospitality businesses such as restaurants and hotels, this 500-employee limit could be applied to each separate business location. Finally, the SBA suspended the ordinary requirement that borrowers must be unable to obtain credit elsewhere as a condition of receiving a PPP loan.

When the program opened, it was clear that the original $349 billion in funds would be insufficient to satisfy demand. On April 16, the original allotment of PPP funds was exhausted. In the intervening days, it became apparent that dozens of public companies had been recipients of PPP funds, the most notable being Shake Shack and Ruth’s Chris, both of which relied on the 500-employee-per-location exception. Given the limited availability of funds, as well as difficulties some smaller businesses had in obtaining loans, the backlash was immediate.

In response, the SBA updated its PPP Q&A to include the following question:

31. Question: Do businesses owned by large companies with adequate sources of liquidity to support the business’s ongoing operations qualify for a PPP loan?

Answer: In addition to reviewing applicable affiliation rules to determine eligibility, all borrowers must assess their economic need for a PPP loan under the standard established by the CARES Act and the PPP regulations at the time of the loan application. Although the CARES Act suspends the ordinary requirement that borrowers must be unable to obtain credit elsewhere (as defined in section 3(h) of the Small Business Act), borrowers still must certify in good faith that their PPP loan request is necessary. Specifically, before submitting a PPP application, all borrowers should review carefully the required certification that “current economic uncertainty makes this loan request necessary to support the ongoing operations of the Applicant.” Borrowers must make this certification in good faith, taking into account their current business activity and their ability to access other sources of liquidity sufficient to support their ongoing operations in a manner that is not significantly detrimental to the business. For example, it is unlikely that a public company with substantial market value and access to capital markets will be able to make the required certification in good faith, and such a company should be prepared to demonstrate to SBA, upon request, the basis for its certification.

The answer went on to state that any borrower that applied for a PPP loan prior to the issuance of this guidance and repays the loan in full by May 7, 2020 will be deemed by SBA to have made the required certification in good faith.

The SBA subsequently released Question #37, which applied the same standard to businesses owned by private companies with adequate sources of liquidity to support the business’s ongoing operations. Finally, on April 28, 2020, Secretary Mnuchin announced that the SBA would conduct audits of all businesses that received greater than $2 million in PPP loans. Accordingly, all businesses should review their situations in light of the guidance in the SBA Q&A and in advance of the May 7 deadline. To date, the SBA has not released any further guidance to specify the conditions needed to certify that the loan request was “necessary,” or to specify the situations where a company has the ability access to other sources of liquidity sufficient to support ongoing operations in a manner “that is not significantly detrimental to the business.”

Regardless of the lack of specific guidance, all companies should document their situation and assumptions at the time the application was prepared and create a “file” to store the documents and data that support the ongoing need for the funds.

Recent history has demonstrated the dynamic, fluid nature of changes with regard to these important relief programs. WK will continue to monitor breaking news and guidance on the CARES Act and the PPP and will provide updates as warranted.

APRIL 30, 2020 UPDATE:

CARES Act

Additional PPP Funding Now Available

The United State Small Business Association (SBA) resumed accepting Paycheck Protection Program (PPP) applications from approved lenders on Monday, April 27t. The PPP has been replenished with $310 billion for banks to loan to businesses in need, of which $60 billion is being set aside for community banks and small lending institutions. If you have questions regarding the PPP funding, please see previously produced alerts on these issues.

Loan Forgiveness Guidance Forthcoming

Guidance on loan forgiveness is still forthcoming from the U.S. Treasury and SBA. Williams-Keepers LLC (WK) continues to monitor the ever-changing nature of business issues related to the COVID-19 pandemic and will provide an update and webinar when guidance is released.

Guidance on Calculating Maximum PPP Loan

On April 24 the Treasury released new interim guidance on calculating the maximum PPP loan by business type. The interim rules provide guidance for self-employed individuals with and without employees on a Schedule C, self-employed individuals with Schedule F income, partnerships, S corporations, C corporations, eligible nonprofit organizations, and limited liability companies (LLC).

The interim rules provide guidance to previously unanswered questions regarding whether self-employed farmers subject to self-employment tax on the Schedule F are eligible for the PPP loan and whether partnership self-employment income is reduced by the employer’s share of self-employment tax on the PPP loan application.

Additional information about the impact of COVID-19 will be provided as the situation develops. We will communicate these alerts via email and on our website at COVID-19 Resource Center.

WK offices to reopen on May 4, follow health-related guidelines

In accordance with a statewide easing of stay-at-home restrictions related to the COVID-19 pandemic, WK will reopen its Columbia and Jefferson City offices on Monday, May 4 with standard 8 a.m. – 5 p.m. hours. The firm will follow guidance provided by health care professionals to ensure the safety of WK associates and its clients when it reopens.

Our intention is for office visits to be as brief as possible for the foreseeable future. In-office visits to both office locations will be limited to the pickup and drop-off of documents and other items. This strategy will serve to promote the continued health and safety of WK associates and the firm’s clients.

We request that office visitors follow several recommendations.

- Please do not enter WK’s offices if you are not feeling well.

- Before you travel, please call ahead to schedule an appointment to drop off or pick up documents so that we can adequately prepare for your arrival. Our lobby areas will include clearly marked instructions about picking up or dropping off information. Those areas will be monitored closely throughout the day.

- While visiting either office, please observe established social distancing guidelines, including hand-washing/sanitizing prior to your visit, maintaining six feet of distance between yourself and others and refraining from handshakes and other physical contact. You may consider wearing a mask, as an extra precaution, when visiting WK.

- We will not host extended client meetings in either office. Additionally, meeting spaces that are typically open for client use and the firm’s restrooms will not be available.

- When possible, please continue to communicate personally with your WK advisor using phone calls, email and, if available, video conference options. Document sharing can also be accomplished through client portals and the firm’s LeapFile system.

We are also taking numerous health-related in-office precautions, as well as precautions for member owners (partners) and associates who will visit client offices beginning May 4.

- In-office work spaces and common areas at WK will be disinfected and cleaned frequently.

- The aforementioned social distancing guidelines will be followed by all WK partners and associates, both in and out of the office.

- Many partners and associates will continue to follow full or part-time work-from-home schedules throughout the month of May, limiting the number of people who are in each office on a daily basis.

- We will follow all firm-recommended guidelines and recommendations made by clients when the firm’s partners and associates visit client offices.

- Our offices allow us to provide more-than-recommended physical space between partners and associates who choose to work in the office.

Consistent with the uncertain nature of the COVID-19 pandemic, WK will continue to monitor changing conditions and health recommendations from local, state and federal authorities. Changes to our current strategy will be made, as needed, and communicated to our clients and communities through email notifications and social media resources.

Please contact your WK advisor for additional information.

APRIL 22, 2020 UPDATE:

More PPP funding will be available: What you should know

A second round of funding intended to provide additional COVID-19 pandemic aid was passed by the United States Senate on Tuesday and sent to the House of Representatives, which according to multiple news outlets is expected to pass the bill as early as Thursday. President Donald Trump is expected to sign the measure, which would provide $484 billion in additional funding quickly following Congressional approval.

For those businesses and self-employed individuals who are eligible for the PPP but missed out on the initial funding, this additional funding will provide a second chance to access the program. Given the limited nature of the funds and the rate at which the initial funds were depleted, Williams-Keepers LLC (WK) recommends completing and submitting applications as soon as possible. Please be aware that nothing in the bill changes the qualifications for eligibility or the calculation of the PPP loan. If you have questions regarding either, please see previously produced alerts on these issues.

The new aid package would include approximately $484 billion in additional funding, including $310 billion to replenish the Paycheck Protection Program (PPP), which last week was exhausted of its initial $349 billion stream. Of the additional $310 billion in PPP funding, $60 billion is set aside for loans to smaller businesses that critics say were more likely to be shut out of the original funding. The bill sets aside $30 billion for loans made by lending institutions with assets between $10 billion and $50 billion. An additional $30 billion is earmarked for loans made by lending institutions with less than $10 billion in assets.

The bill also adds $50 billion in funding for Economic Injury Disaster Loans (EIDL) and $10 billion in funding for Emergency EIDL Grants. Both programs had also exhausted prior appropriations. The bill also expands the EIDL and Emergency Grant programs to allow agricultural enterprises to participate.

For those that have already secured PPP loans, nothing in this bill changes what we know or don’t know about how to qualify for loan forgiveness. For a discussion of these issues, please read our white paper on this issue.

In anticipation of the approval of the second round of funding, WK Member Owners Mark Gingrich, CPA, J.D. and Jeremy Morris, CPA participated in a podcast this week with Clear Vision Development Group Founder and Senior Partner Tony Richards about the first round of Payroll Protection Program (PPP) funding and the ways business owners can ensure their PPP loans are forgivable.

WK continues to monitor the ever-changing nature of business issues related to the COVID-19 pandemic and will provide additional updates, as needed.

WK offices remain closed

In accordance with local and statewide health directives, WK’s offices will remained closed to in-office visitors until Monday, May 4, 2020.

To schedule an appointment using other methods please contact with your WK advisor at either (573) 442-6171 (Columbia) or (573) 635-6196 (Jefferson City).

APRIL 15, 2020 UPDATE:

New Paycheck Protection Program Guidance Issued :

On Tuesday, April 14, the U.S. Small Business Administration (SBA) released an Interim Final Rule that provided additional guidance for implementation of the Paycheck Protection Program (PPP). Highlights from the guidance follow.

How Do Self-Employed Individuals File for PPP Loans?

Although the PPP program was open to self-employed individuals beginning on April 10, the SBA had not yet released guidance on how that process would work. The Interim Final Rule states that self-employed individuals who meet the following requirements are eligible for PPP loans.

- They were in operation on February 15, 2020.

- They had self-employment income, such as an independent contractor or sole proprietor.

- They are a resident of the United States.

- They have filed or will file a 2019 Form 1040 Schedule C.

The maximum loan amount for a self-employed individual will be calculated based on:

- 2.5 times average monthly payroll costs, if the business has employees, for 2019; plus

- 2.5 times average monthly 2019 Schedule C net profit; plus

- the outstanding amount of any Economic Injury Disaster Loan (EIDL) made between January 31, 2020 and April 3, 2020 that the taxpayer seeks to refinance as part of the PPP.

For purposes of this calculation, 2019 average monthly Schedule C net profit equals total 2019 Schedule C net profit divided by 12. This means any business reported on a 2019 Schedule C cannot claim any PPP benefit if it reported a loss in 2019, and the Treasury does not adjust for non-cash expenses such as accelerated tax depreciation. Businesses with in-progress 2019 tax returns that will include one or more Schedule C will want to consider the impact of 2019 depreciation elections on the availability of PPP funds.

A 2019 Schedule C must be included with the PPP application, regardless of whether a taxpayer has filed a 2019 return with the IRS. As it relates to loan forgiveness, the loan amounts can be used to pay the standard covered costs, including employee payroll costs, mortgage interest payments, business rent payments and business utility payments.

In addition, the loan can be used as owner compensation replacement, which is calculated as eight weeks’ worth of 2019 profit, calculated as 8/52 multiplied by 2019 Form 1040 Schedule C net income. Thus, the same 2019 Schedule C income used to calculate the loan will also be used to calculate loan forgiveness.

Is This Process Applicable to Partners in a Partnership?

The Interim Final Rule clarifies that partners in a partnership may not submit separate PPP loan applications for themselves as self-employed individuals. Instead, the self-employment income of general active partners may be reported as a payroll cost, up to $100,000 annualized, on a PPP loan application filed by, or on behalf of, the partnership.

This provides a challenge for those partnerships that have already filed for a PPP loan that excluded partner income from the loan calculation because of the interpretation that partners were self-employed individuals that were required to file separately.

What Clarifications Did the Guidance Provide on Loan Forgiveness Questions?

As noted in WK’s PPP Loan White Paper issued on April 13, there are many items that require clarification from the United States Department of the Treasury, particularly as it relates to the calculation of loan forgiveness. The Interim Final Rule provides insight on some of these issues.

Is interest paid on loans secured by personal property a cost that will produce loan forgiveness, i.e, Good Costs?

The Coronavirus Aid, Relief, and Economic Security (CARES) Act states that costs subject to loan forgiveness include payments of interest on business mortgage obligations on real or personal property. The Interim Final Rule provides as examples of qualified mortgage expenditures “interest on your mortgage for the warehouse you purchased to store business equipment or the interest on an auto loan for a vehicle you use to perform your business.” Thus, interest paid on business loans secured by personal property appear to qualify as Good Costs for loan forgiveness.

In a similar way, business rent payments related to both real and personal property also appear to be Good Costs. The examples given in the Interim Final Rule include rent payments on a warehouse where business equipment is stored and rent payments on the vehicle used to perform business.

Transportation is included in the list of utilities that qualify as Good Costs. What specific transportation costs count?

The examples given in the Interim Final Rule for Good business utility costs are “the cost of electricity in the warehouse you rent or gas you use driving your business vehicle.” Thus, utilities used to power a vehicle used in the business (e.g., electricity or gas) appear to qualify as Good Costs.

Which Questions Remain Unanswered?

The Interim Final Rule provides guidance for Schedule C taxpayers but is silent on the eligibility of Schedule F farm income or Schedule E rental income to be included in the PPP. Does this silence imply that those with farm income on a Schedule F cannot apply for a PPP loan based on their farm income, or will the SBA issue guidance specific to farm income? Assuming the farm income is similar to Schedule C income in that it is treated as “self-employment” income, can we apply the Schedule C rules to the Schedule F without the need for additional guidance?

Similarly, does the silence relative to rental income reported on a Schedule E imply that those with rental income on a Schedule E cannot apply for a PPP loan? The additional complication related to rental income is that this income is not treated as “self-employment” income for other purposes in the Internal Revenue Code. Does the repeated and consistent references to “self-employment” income in the Interim Final Rule imply rental income does not qualify for the PPP? Does this answer change if the taxpayer is a “materially participating real estate professional?”

The Interim Final Rule only provides guidance for those with self-employment income in 2019. The SBA has stated it will issue additional guidance for those individuals who were not in operation in 2019 but were in operation on February 15, 2020, and who will file a 2020 Schedule C.

Finally, this Interim Final Rule does not answer the myriad of questions related to the potential reduction of forgiveness due to a reduction in employees or a reduction in employee pay (as well as the related “rehire” provisions). For a more detailed examination of these issues, please refer to our white paper on this topic.

Today’s Conclusions

Consistent with so many other aspects of recently passed federal aid legislation, including the Families First Coronavirus Relief Act (FFCRA) and CARES Act, the release of Tuesday’s guidance provides many important clarifications but also leaves open several key questions. WK advisors continue to seek answers to these questions, and updates will be provided when additional information is available.

APRIL 13, 2020 UPDATE:

Using Paycheck Protection Program Loans Effectively:

PPP Loan White Paper here.

A summary of the things we know today is included in this white paper. It should be noted that items listed in underlined italics indicate a subject that requires further clarification from the United States Department of the Treasury.

COVID-19 Business Planning: Updated 04.11.20

Interpreting ways clients can benefit from the recently passed Coronavirus Aid, Recovery, Economic Security (CARES) Act and the Paycheck Protection Program (PPP) was among Williams-Keepers LLC’s (WK) top priorities this week. Although many aspects of these two wide-reaching government relief packages are clear, questions remain about key provisions.

WK advisors continue to monitor answers to these important questions and the ways the CARES Act will impact businesses of many different sizes and structures. Additional information will be distributed, as it becomes available, during the week of April 13.

A summary of the things we know today follows.

Applying for the PPP? Here’s what you need

If you plan to apply for a potentially forgivable loan under the PPP, you will need to have specific documentation to complete your application. Please see the checklists at the bottom of this page to learn more about what small businesses and not-for-profit organizations should gather before applying.

How to Claim NOL Carrybacks and Enhanced Carryforwards

The Coronavirus Aid, Recovery, and Economic Security (CARES) Act relaxes the limitations on a company’s use of losses. As part of the Tax Cuts and Jobs Act (TCJA), businesses were no longer able to carry net operating losses (NOL) back to a prior tax year to immediately recover previously paid tax. Additionally, NOLs incurred after 2017 that were carried forward were limited to offsetting a maximum of 80 percent of taxable income in the carryover year.

The CARES Act allows NOLs occurring in a tax year beginning in 2018, 2019 or 2020 to be carried back five years, and losses carried to 2019 and 2020 may be used to offset 100 percent of taxable income, as opposed to 80 percent under TCJA. These changes will allow companies to utilize losses and amend prior year returns immediately. The IRS released new guidance this week to help with the mechanics of carryback filings. However, the unfortunate truth is the IRS’s limited capacity to process these claims during the COVID outbreak will likely slow resulting refunds.

For a specific example of how this might work, please visit this link.

IRS extends Q2 estimated payment due date, more tax deadlines for estates, trusts, other entities

This week the Internal Revenue Service (IRS) extended more tax deadlines to cover individuals, estates corporations and other taxpayers, including non-profit entities, as a result of the COVID-19 pandemic.

Following up on previous action related to the extension of quarterly tax deadlines, the IRS has extended the quarterly estimated payments for both Q1 and Q2 to July 15, 2020. Previous guidance only provided for an extension of time to pay Q1 estimates.

These extensions also include a variety of tax form filings and payment obligations that are due between April 1, 2020 and July 15, 2020, including estimated tax payments due June 15 and the deadline to claim refunds from 2016. The Notice also suspends associated interest, additions to tax and penalties for late filing or late payment until July 15, 2020.

This relief is automatic. Taxpayers do not have to call the IRS or file any extension forms or send letters or other documents to receive this relief.

A complete list of tax filings deadlines is available on the IRS website at this link.

Details Lacking as PPP Expands to Include Self-Employed Taxpayers, Independent Contractors

On Friday, April 10 the Small Business Administration (SBA) opened the process that includes self-employed individuals and independent contractors. A link to information provided by the SBA is included here.

It has been widely reported that the program is off to a rocky start, with uncertainty among banks about how to administer the loan application process and other ambiguities.

WK will provide a more detailed evaluation of how this aspect of the PPP might apply to self-employed taxpayers and independent contractors when more complete details are available. We are finding many banks will be holding PPP applications for independent contractors and self-employed individuals until Treasury and SBA release guidance.

New lending programs available for larger businesses, local governments

The United States Federal Reserve announced on Thursday, April 9 a new program to help larger businesses and local governments during the COVID-19 crisis.

According to Reuters, the program includes “… four-year loans to companies of up to 10,000 employees and begin to directly lend to state governments and more populous counties and cities to help them respond to the crisis.”

Additional information about the program is available at this link.

WK is working to analyze the ways this new program might benefit its clients, and additional information will be available next week.

APRIL 3, 2020 UPDATE:

COVID-19 Business Planning

How Does Your Business Respond?

COVID-19, though medical in nature, has had a devastating impact on businesses and the individuals who own or are employed by those businesses. There is much confusion and concern, and business owners find themselves asking “What is the best course of action?” as it relates to maintaining long-term business viability and ensuring the welfare of those they employ.

There are, unfortunately, no easy answers, and the optimal decisions will be different in each situation. In addition, business owners have new tools at their disposal, in the form of provisions found in the Coronavirus Aid, Recovery, and Economic Security Act (CARES Act), and the Families First Coronavirus Relief Act (Families First Act). WK has put together some tools and strategies to effectively navigate common situations businesses are facing. Click here to read more.