News

Federal act eliminates some Social Security claiming strategies

The Bipartisan Budget Act of 2015, signed by President Obama on November 2, 2015, eliminated a number of Social Security claiming strategies. The bill refers to these claiming strategies as “unintended loopholes” that were being exploited by some individuals and families to significantly increase their lifetime benefits.

[ezcol_2third]

Social Security recipients are generally eligible for two potential benefits: the benefits based on their own work history (workers benefit) or the benefits based on their spouse’s work history (spousal benefit). The amount they receive is the greater of the workers benefit or the spousal benefit.

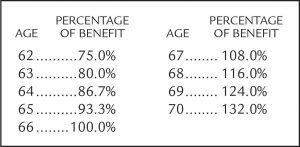

For workers born between 1943 and 1954, the full retirement age (FRA) is 66. An individual’s retirement benefits will be permanently reduced if the benefits begin before the retiree reaches their FRA. On the other hand, retirement benefits will be permanently increased if the individual delays receiving benefits until after reaching the FRA. The chart shows the impact on the benefits received based on when the retiree chooses to receive benefits.

For workers born between 1943 and 1954, the full retirement age (FRA) is 66. An individual’s retirement benefits will be permanently reduced if the benefits begin before the retiree reaches their FRA. On the other hand, retirement benefits will be permanently increased if the individual delays receiving benefits until after reaching the FRA. The chart shows the impact on the benefits received based on when the retiree chooses to receive benefits.

The two claiming strategies impacted by the Bipartisan Budget Act of 2015 include:

- File and Suspend

- Restricted Application

File and Suspend Method

Strategy Defined. The Social Security Administration allows a worker that has attained full retirement age to file and suspend their benefits. This allows the retiree’s benefits to grow until a later date that the retiree elects to receive them. The strategy has two important features.

By filing and suspending, a worker makes his dependents (spouse, child) eligible to receive benefits to which they are entitled. A dependent cannot receive benefits on the worker’s record until after the worker has filed for their own benefits. By electing to file and suspend, the retiree allows their spouse to take advantage of the restricted application (discussed below).

Additionally, the file and suspend method offers a retiree a great deal of flexibility. If at a later date the retiree regrets the decision to suspend his benefits (e.g. his life expectancy is reduced), he can receive a lump sum benefit retroactively to the month in which he filed.

Effect of Bipartisan Budget Act of 2015. The Act effectively eliminates this opportunity for claims filed on or after April 30, 2016 (180 days after enactment). Those who have been using this method or other eligible individuals who file to claim benefits under this method within the 180 days of the Act’s passage should not be affected.

Action. Individuals who have reached full retirement age or who will do so by April 29, 2016, and who would like to understand how this strategy might impact their Social Security benefits should contact their WK advisor.

Restricted Application Strategy

Strategy Defined. Under this strategy, a spouse reaching full retirement age who is eligible for both a spousal benefit (based on his or her spouse’s earnings) and a retirement benefit (based on his or her own earnings) could file a restricted application for spousal benefits only, then apply for retirement benefits based on his or her own earnings record at a later date. This would allow the retirement benefit to grow at the rates shown in the previous tables and allow the retiree to collect spousal benefits in the meantime.

Effect of Bipartisan Budget Act of 2015. For those who turn 62 after 2015, the Act eliminates the ability to file a restricted application for only spousal benefits. Individuals who are age 62 or older in 2015 should still be able to use the restricted application method for spousal benefits only upon reaching full retirement age.

Action. Anyone born before January 1, 1954, will still be able to do a Restricted Application for spousal (or divorced ex-spouse) benefits, even if the filing doesn’t occur until years from now.

Example

The following example shows file and suspend and a restricted application strategy can work together to dramatically increase Social Security benefits.

Jeremy and his wife Beth are both 66 and have reached full retirement age (FRA). Jeremy has an FRA benefit of $1,500 and Beth has an FRA benefit of $800. The happy couple would like to maximize their benefits.

Jeremy would like to delay receiving his Social Security benefits until age 70 to maximize the amount of benefits he will receive. His benefits will increase by 8% each year he delays receiving benefits until age 70. The couple would benefit from Jeremy filing and suspending. This would open the door for Beth to file for spousal benefits. Note that it is required that one spouse must have established a filing date in order for the other spouse to receive spousal benefits.

Beth can now file for spousal benefits and receive 50% of Jeremy’s FRA benefit, which is equal to $750 ($1,500 x 50%). This allows Beth’s benefits to grow at a rate of 8% a year. At age 70 she can then elect to receive her own benefits, which now equal $1,056 ($800 x 132.0%) instead of the $750 spousal benefit.

If you’d like to learn more about the changes in Social Security claiming strategies, please contact your WK advisor at (573) 442-6171 or (573) 635-6196.

[/ezcol_2third] [ezcol_1third_end]

OTHER STORIES FOR YOU

HOW RETIREMENT AGE IMPACTS SOCIAL SECURITY AND OTHER BENEFITS. As we age, most birthdays are just about getting another year older. But as we reach retirement, birthdays take on new meaning: various ages signify new options available to collect Social Security benefits and other retirement income.

NEW LAW CHANGES SOME TAX RETURN DUE DATES. A number of tax return due dates were changed by provisions of a federal law extending highway funding. While that might seem like an odd bill for tax changes, it became law of the land on July 31, 2015, when President Obama signed the “Surface Transportation and Veterans Health Care Choice Improvement Act of 2015” (the Act).

TRADITIONAL VS. ROTH IRAS – WHICH IS BEST FOR YOU? Choice is a good thing, but informed choice is even better! When it comes to selecting a retirement savings vehicle, you can choose between traditional and Roth Individual Retirement Accounts (IRAs), which have unique advantages and tax consequences. To get the most benefit from your savings, carefully evaluate the differences between traditional and Roth IRAs, consider your personal circumstances, and choose the IRA that works best for you.

[/ezcol_1third_end]